Every surrogacy agency's website reads the same. Transparent. Ethical. Family-first. Compassionate. If you're comparing four agencies on a shortlist, the homepages won't tell you anything useful.

What actually separates agencies are the operational details that never make it onto the website — how they collect their fees, who reviews the medical records, what happens when a match falls through, who handles the insurance paperwork. These are the details that intended parents only discover after they've already signed.

This article isn't a general checklist. It's a list of the six traps we see intended parents fall into most often — not from market research, but from the steady stream of IPs who came to Ivy after a setback at another agency. The stories overlap so consistently that we stopped being surprised years ago.

Most of the traps below end with a specific question you can bring to any consultation call. Ask the same question at every agency on your shortlist, and compare how specific the answers are. A vague answer is itself an answer.

Key Takeaways

- Never pay the agency fee before being matched. The single biggest trap is signing a retainer and paying upfront just to join a waiting list. Once you've paid, you've lost your leverage.

- The agency itself should be screening medical records before the IVF doctor sees them. If no one on the team has the clinical training to read records, failed matches become much more likely.

- Re-match priority matters more than re-match policy. Find out whether re-match clients get first access to new candidates, or wait in the same queue as new revenue.

- In-house legal and in-house escrow are non-negotiable red flags. Both create conflicts of interest. One has produced the worst fraud cases in U.S. surrogacy history.

- Insurance has two blind spots, not one. Many agencies handle the surrogate's insurance poorly and don't handle newborn insurance at all — a six-figure problem for international intended parents.

- Be skeptical of dramatic success rates. They almost always measure cumulative outcomes across unlimited attempts, and they're not really about the agency anyway.

Trap 1: When the Agency Fee Is Actually Due

This is the single biggest trap. It goes first because it causes more damage than any other issue on this list.

Most U.S. surrogacy agencies ask intended parents to sign a retainer and pay the agency fee — in full or in part — right after the first consultation call, before you've been matched with a surrogate, before you've seen a single profile, sometimes before you've been told how long the wait will be. Once you've paid, you're added to a waiting list that can stretch six to twelve months. For some agencies, longer.

The damage from this model is structural, not occasional. The moment the fee is paid, you transfer control of your own journey:

- You don't decide when you get matched. The agency decides the sequence.

- You don't decide who you get matched with. The agency decides which profiles to show you, and when.

- If eight months go by and nothing has moved, you can't switch agencies without writing off tens of thousands of dollars in non-refundable fees.

- Worst of all, the agency's financial incentive is no longer aligned with you. You've already paid. Their sales team is compensated on bringing in new clients, not on serving old ones. You quietly become someone to manage, not someone to serve.

There are three possible timing points for the agency fee, from worst to best:

1. Due at signing, before match. The agency collects its fee — in full or in part — before you've been matched with anyone. You have no leverage, no information about your specific journey, and no exit. This is the worst model, and unfortunately it's also the most common one among large U.S. agencies.

2. Due at match, before screening. You pay when a candidate is identified. Some agencies collect this payment after the IVF doctor has reviewed the candidate's medical records; some collect it even before that review. Either way, she has not yet undergone the in-clinic physical exam and lab work, and she has not yet completed the psychological evaluation. This is better than Model 1 — at least you know who you're being matched with — but you're still paying for an outcome that isn't yet guaranteed. If the physical exam or psychological evaluation fails, you're tied to the agency for the re-match, and you've already given up your financial leverage.

3. Due after the surrogate clears medical and psychological screening. You pay only when the match has actually held up under scrutiny — when the IVF doctor has reviewed her medical records, cleared her through an in-clinic physical exam and lab work, and when the psychological evaluation has also passed. This is a very different milestone from a records review alone. A records review happens on paper, before the surrogate ever sets foot in the clinic; medical clearance comes later, after the physical exam and lab work confirm she's actually fit to carry. Only at that point does the journey have real traction, and only at that point is the agency's fee genuinely earned. This is the only model that keeps the agency's incentives aligned with yours all the way through the pre-screening phase, and it's why Ivy charges the agency fee only after the surrogate passes both screenings.

You cannot realistically expect every agency to operate on Model 3 — most won't. But you should never, under any circumstances, sign with an agency operating on Model 1. The minimum acceptable standard is Model 2: no money before you've been matched with a specific, named candidate.

Bring this to consultation:

"When exactly is the agency fee due — at signing, at match, or after the surrogate clears medical and psychological screening? Please show me the clause in the sample contract."

Walk away if you hear:

- "We require a retainer to place you on the waiting list."

- "Fees are due within 30 days of signing, before matching begins."

- "Everyone pays upfront — it's how the industry works."

- Any refusal to put the fee-timing clause in writing.

Trap 2: Who Actually Reviews the Surrogate's Medical Records

This trap is less famous than Trap 1, but it causes the same kind of damage: wasted months, failed screenings, and re-matches that should never have been necessary.

Before a surrogate candidate is introduced to an intended parent, her complete medical records should already have been reviewed by someone on the agency's team who is actually qualified to read them. That means someone who can interpret prenatal records, delivery notes, C-section operative reports, ultrasound reports, and chronic-condition management notes. Not everyone on an agency team can do this. Most people can't.

When this pre-screening step is skipped or done badly, two things go wrong:

The agency has no one who can read medical records. The case management team is made up of coordinators and social workers — empathetic, well-meaning, but without the clinical training to recognize the details that matter in a prior pregnancy. A history of preeclampsia with specific severity markers. Gestational diabetes that was technically "managed" but poorly controlled on the actual lab trends. A postpartum hemorrhage noted briefly in the delivery report. A thyroid condition whose medication history tells a different story than the summary line. None of these jump off the page unless someone trained to read obstetric records is actually reading them. So the agency simply forwards whatever the surrogate provides directly to the IVF doctor and hopes for the best.

The agency skips it on purpose. More cynically, some agencies push a candidate toward matching before her medical records are even fully collected — because matching is when the retainer gets signed and the agency fee gets paid. Every week of delay is a week of revenue lost. A candidate who might fail the IVF doctor's review two months later is still a candidate who generates fee revenue today.

In either case, the outcome is the same: the risk that the IVF doctor rejects the candidate is much higher than it needed to be. The match collapses, the clock resets, and two or three months are gone. A proper internal pre-screening doesn't guarantee the IVF doctor will approve every referred candidate — no pre-screening can. But it meaningfully lowers the rejection rate, and it ensures that when a rejection does happen, it wasn't for something the agency should have caught on day one. If the agency is also operating on Trap 1's Model 1, you've now paid for a journey that was predictably unlikely to work.

The correct workflow looks like this:

- The agency collects the candidate's complete obstetric history — all prior pregnancies, with full prenatal records and delivery notes for each, plus records of any chronic conditions, current medications, and recent physical exam results.

- Someone on the agency's team with clinical training reviews those records and screens for disqualifiers that a trained eye can see.

- Candidates with clear red flags are filtered out before they're ever shown to an intended parent.

- Only candidates who pass internal pre-screening are referred to the IP's IVF doctor for medical records review.

- If the IVF doctor approves the records, the candidate proceeds to the in-clinic physical exam and lab work. In some cases, the IVF doctor may also request an additional Maternal-Fetal Medicine (MFM) consultation, particularly when there are risk factors in the obstetric history. Medical clearance only comes after all of this is complete.

At Ivy, this internal pre-screening is done by our CEO Chris, who has a clinical nursing background, over two decades of experience across the broader healthcare industry, and direct operational experience at an IVF clinic. We mention this not to advertise but because you should be looking for a comparable answer at every agency you interview — a specific person, with a specific clinical background, doing a specific review. "Our team screens carefully" is not an answer.

Bring this to consultation:

"When you send me a surrogate candidate's profile, have her medical records already been collected in full? Has someone on your team actually reviewed those records before introducing her to me? Who on your team does that review, and what is their clinical background? Can you walk me through a case where a candidate was filtered out at the internal pre-screening stage, and explain why?"

Walk away if you hear:

- "Our case managers handle the screening."

- "The IVF doctor will do the medical review." (This means the agency does no pre-screening of its own.)

- Vague answers with no named person and no named clinical qualification.

- An inability to describe the kinds of issues they catch at internal pre-screening, in specific clinical terms.

Trap 3: Where You Stand in Line After a Re-Match

Nobody wants a re-match. But in a market where qualified surrogate candidates are scarcer than intended parents, re-matches happen — candidates withdraw, screenings fail, transfers fail, and sometimes an IP and a surrogate simply aren't the right fit after the match meeting. Over a long enough timeline, every agency deals with re-matches.

The trap isn't whether re-matches happen. The trap is what the agency does when a new surrogate candidate becomes available, and the agency has to decide: does this candidate go to an existing client who needs a re-match, or to a new client who just signed a retainer?

The honest answer most agencies give, if you push them hard enough, is: they wait in the same queue. Everyone gets treated "equally." On the surface this sounds fair. In practice, it isn't.

Here's why. Matching a new candidate with an existing re-match client generates no new revenue — the agency fee for that journey was already paid. Matching the same candidate with a new client generates a new agency fee. From a pure cash-flow perspective, the agency has every reason to prioritize the new client. And because both clients are technically "in the same queue," no one can accuse the agency of unfairness when the new client happens to be matched first. The unfairness is hidden inside the sequencing.

The intended parents who need re-matches are usually the ones who have already been through something hard. A failed transfer. A surrogate who withdrew after weeks of coordination. A screening that revealed a disqualifying condition late. These families have already spent months in the system, absorbed the emotional cost, and in many cases absorbed real medical expenses. They are also, typically, the most financially and emotionally depleted clients on the agency's roster. Putting them "in the same queue" as brand-new clients looks fair on the surface but functionally puts the most vulnerable clients at the back of the line — because new clients bring new revenue, and newly available candidates naturally flow toward the clients who generate fresh fees.

The right policy is the one that costs the agency money in the short term: re-match clients get priority. When a new qualified surrogate enters the pool, she is offered first to intended parents who are waiting on a re-match, before any new client is matched. The agency loses new-client revenue in the short term and protects the integrity of existing journeys in the long term. This is the policy Ivy operates on, and we mention it here because it's the simplest possible test of whether an agency's "family-first" language describes its actual financial behavior or its marketing copy.

Bring this to consultation:

"If I need a re-match for any reason, do I go back to the end of the line with new clients, or do re-match clients get priority access when a new surrogate becomes available? What's your average re-match waiting time over the past 12 months?"

Walk away if you hear:

- "We treat all clients equally." (This is the polite version of "you go to the back of the line.")

- "Re-matches are handled on a case-by-case basis." (No policy is a policy.)

- No data on average re-match waiting times.

Trap 4: In-House Legal and In-House Escrow

The next two traps are well-known enough in the industry that we've written separate deep-dive articles on each one. Here we'll keep it short and link out.

In-house legal. Some agencies advertise their "in-house legal department" as a convenience. It isn't a convenience — it's a conflict of interest. An attorney employed by the agency cannot independently represent you against the agency's own interests, and California Family Code §7962 explicitly requires that intended parents and gestational carriers have independent legal counsel. If an agency offers to "handle the legal work internally," they are either operating in a state without clear surrogacy legislation, or betting that you won't ask the question. Either way, the answer is no. See our full article on why in-house legal is a red flag for intended parents.

In-house escrow. Worse. In 2009, a California agency called SurroGenesis, operating an in-house escrow system, embezzled over $2 million in client funds. The case directly produced California Family Code §7961, which now requires non-attorney surrogacy facilitators to hold client funds in licensed independent escrow or attorney-managed trust accounts. Even today, some large agencies still operate in-house escrow divisions or "sister companies" in states with weaker regulation. And even when an independent escrow provider is in place, some agencies still ask clients to wire the funds to the agency first — which defeats the purpose entirely. The rule is simple: your money goes directly to a licensed third-party escrow or attorney trust account, never through the agency. See our full article on why you should avoid in-house escrow in surrogacy arrangements.

Bring this to consultation:

"Is your legal counsel in-house or independent? Is your escrow account held by a licensed third-party escrow company or attorney trust account, and will I wire funds directly to that provider?"

Walk away if you hear:

- "We have an in-house legal team — it's faster."

- "We operate our own escrow — it's more efficient."

- "You'll wire funds to us first, and we'll forward them to escrow."

Any one of these answers is a full stop.

Trap 5: The Insurance Double Blind Spot

Insurance is where agencies fail intended parents in two completely different ways, at two different stages of the journey. Most IPs only discover the second failure after the baby is born — far too late to fix.

5.1 The surrogate's health insurance

Most U.S. health insurance plans contain a "surrogacy exclusion clause" — language that specifically excludes coverage for a pregnancy carried on behalf of someone else. These clauses are buried deep in the policy documents and they are not always obvious even to people who work in insurance. Verification of an existing plan is part of what a licensed insurance broker does, but there's a second, equally important check: whether the policy contains lien provisions that allow the insurer to recover claim payments from the intended parents after the fact. A lien can turn what looks like a covered pregnancy into a significant unexpected expense for the IP months after delivery.

In practice, though, verifying an existing plan is usually the smaller part of the job. More often, the surrogate either has no health insurance at all, or her existing plan has a clear surrogacy exclusion, and the real work is helping her enroll in a surrogacy-friendly ACA marketplace plan — selecting a carrier and plan tier whose network and benefits structure actually work for a surrogacy pregnancy, and timing the enrollment to align with the ACA's open enrollment window (or a qualifying special enrollment period, if one applies).

This is not something a case manager can do by reading a summary of benefits. It requires a licensed insurance broker who specializes in surrogacy. When the agency skips this step or assigns it to a non-specialist, the failure mode is always the same: everyone assumes the surrogate's coverage is fine, the journey proceeds, and somewhere in the second or third trimester a claim gets denied — or a lien is triggered. At that point the intended parents are left scrambling, often at a significantly higher cost than if the insurance had been planned for from the beginning.

5.2 Newborn insurance — the real blind spot

This is the failure mode that catches international intended parents worst, and it is shockingly common: many agencies simply tell intended parents, up front, that newborn insurance is not part of their service. They'll help with the surrogate's insurance (sometimes), but once the baby is born, it's the parents' problem.

For domestic U.S. parents, this is manageable. Birth is a Qualifying Life Event, and a newborn can be added to the intended parent's existing employer or marketplace plan within 30 days of birth, with coverage usually retroactive to the date of delivery. It's not trivial paperwork, but it's solvable.

For international intended parents, it's a trap that can cost six figures. International IPs are not U.S. residents, cannot use employer coverage, and have to navigate a narrow set of options:

- Cash pay. Fine if the baby is healthy and discharged in 24–48 hours. Catastrophic if the baby needs NICU care. NICU stays in the U.S. routinely exceed $300,000 and can exceed $500,000.

- Specialty newborn insurance, underwritten by a small number of specialty carriers. These policies cover NICU but have strict purchase deadlines — typically 28 to 30 weeks of gestation. Miss the window and the option is gone.

- ACA marketplace enrollment after birth, which is possible case-by-case in certain states using birth as a Qualifying Life Event. Eligibility varies by state, most agencies don't help with it, and any medical care before enrollment remains the parents' responsibility.

About 10% of U.S. newborns need NICU care. For IVF singletons the rate is slightly higher, and for twins it jumps to around 60% preterm delivery risk. The idea that a surrogacy journey is "done" the moment the baby is born is a dangerous fiction. An agency that doesn't help you plan for newborn insurance before the transfer cycle is an agency that has decided the hardest and most expensive part of the journey isn't their problem.

For the full picture on NICU costs, purchase deadlines, and the differences between domestic and international options, see our complete guide to surrogacy newborn insurance.

Bring this to consultation:

"Do you work with a licensed insurance broker who specializes in surrogacy — someone who can verify an existing plan's exclusions and lien provisions, and, if needed, help enroll the surrogate in a surrogacy-friendly ACA plan during the appropriate enrollment window? And do you help international intended parents arrange newborn insurance — including specialty policies and ACA enrollment?"

Walk away if you hear:

- "The surrogate's insurance will cover everything."

- "Newborn insurance isn't part of our service."

- "We recommend clients sort that out on their own."

- An inability to name a single specialty newborn insurance product or broker partner.

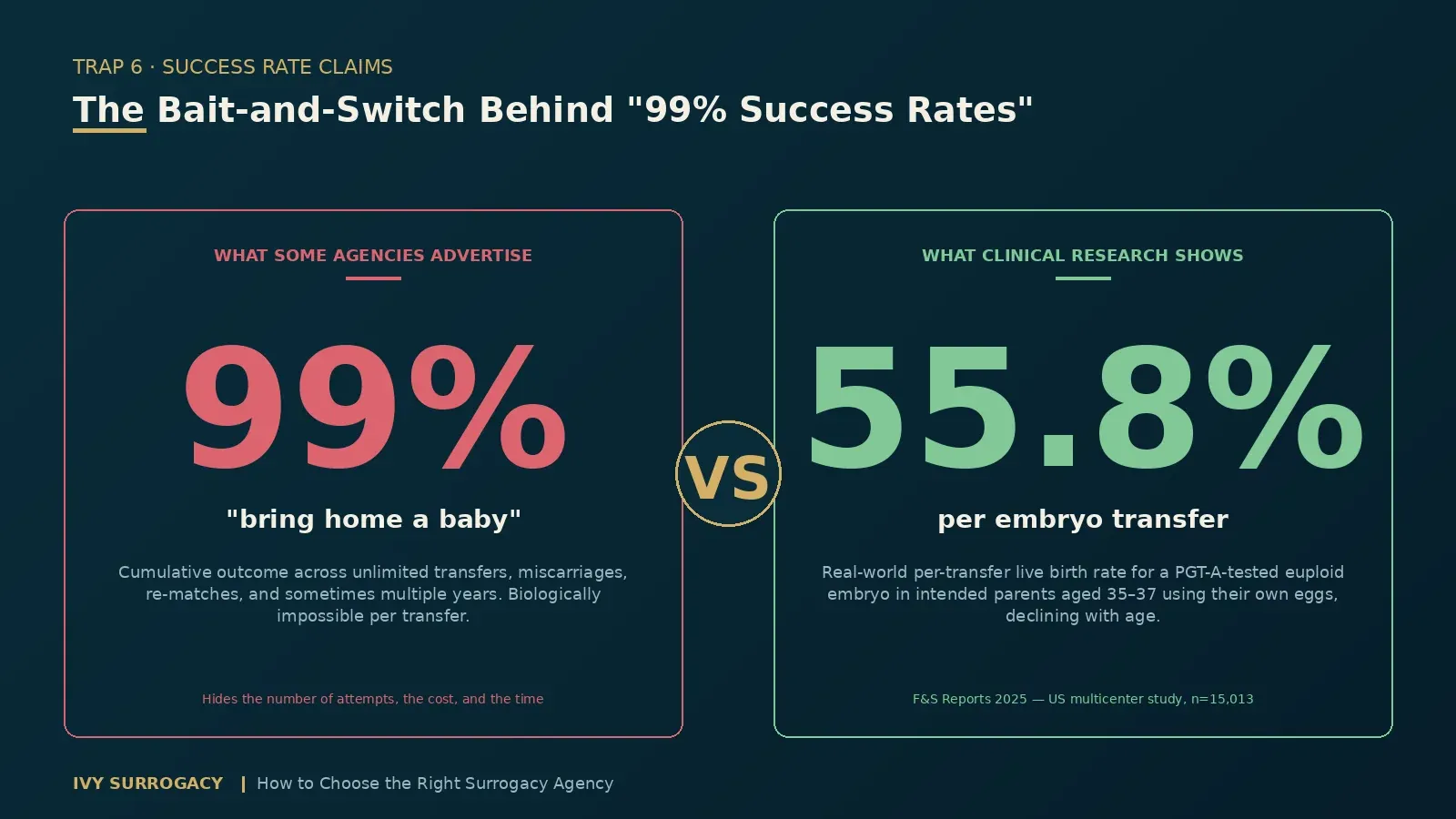

Trap 6: How Agencies Hide Behind "Success Rate" Claims

Some of the largest U.S. surrogacy agencies advertise success rates above 95%. A few publish numbers as high as 99%. On the surface, those figures look like a promise. In practice, they are a textbook bait-and-switch, and anyone who understands IVF outcomes should be skeptical of them immediately.

Here's the problem. When intended parents read "99% success rate," what they hear is: if I start a journey here, there's a 99% chance the first transfer works and we go home with a healthy baby. That is not what the number means. What those agencies are actually measuring — usually described with language like "over 99% of our parents eventually bring home a baby" — is the cumulative outcome across an unlimited number of attempts: multiple embryo transfers, miscarriages, terminations, surrogate withdrawals, re-matches, and in some cases multiple years of effort. Almost any agency that keeps clients in the system long enough will eventually deliver a baby, because the IP keeps trying. "Did you eventually bring home a baby" and "what is the likelihood any given step will succeed" are two completely different questions.

The real benchmark comes from reproductive medicine, and it's backed by hard data. A 2025 U.S. multicenter study published in F&S Reports, analyzing 15,013 single euploid frozen embryo transfers, found that for intended parents aged 35–37 using their own eggs, the per-transfer live birth rate was 55.8% — declining linearly with age from there. That is the real-world performance of a PGT-A-tested, chromosomally normal embryo in mature U.S. fertility clinics, and it's from one of the better age groups. Untested embryos are lower. No serious fertility specialist would claim 99% on a per-transfer basis, because the underlying biology does not support it. When an agency publishes a number that is mathematically incompatible with the clinical reality, they are not telling you about outcomes. They are telling you about marketing.

(A side note: if you want to understand how to actually read IVF success rate data — including which metrics matter, how to compare clinics fairly, and what the CDC's published numbers really mean — we've written a dedicated guide on how to interpret CDC IVF success rates.)

Re-read what a 99% "bring home a baby" rate is actually hiding. It's hiding how many transfers it took. It's hiding how many miscarriages happened along the way. It's hiding how many re-matches were required. It's hiding how long the journey took. It's hiding how many times the IP had to pay for another cycle. The agency still counts the outcome as a win — and from a certain point of view, it is. But the journey behind that headline number may have been far more painful and far more expensive than the intended parent was led to expect.

There's a deeper point here, and it's the one that matters most: success rates in surrogacy are not really about the agency. Whether an embryo implants and develops into a healthy baby is determined by factors the agency has almost no control over — the intended parents' age (or the egg donor's age) at the time of egg retrieval, the skill of the IVF doctor, the quality of the embryology lab, the genetic quality of the embryos themselves. The intended parents choose the IVF clinic. The intended parents (or their donor) provide the eggs. The agency does not perform the transfer, does not grow the embryos, and does not control the biology. Every gestational surrogate who reaches a transfer has, by definition, already passed her medical screening and met the IVF clinic's criteria for embryo transfer — otherwise the transfer would not happen. The variable that the agency is most responsible for is upstream of all this: matching the IP with a qualified, healthy candidate, and supporting the journey logistically. That work matters enormously. But it is not what determines whether a given transfer results in a live birth.

So when you see an agency advertising a dramatic success rate, the right reaction is not "let me ask them how they calculated it." The right reaction is to be skeptical of the agency itself. Any agency willing to misrepresent the most basic biology of IVF in its marketing is telling you something about how it will communicate with you for the next 18 to 24 months. Trust the agencies that don't make claims they cannot honestly support.

Walk away if you hear:

- "We have a 99% success rate." (Biologically impossible on a per-transfer basis.)

- "Over 99% of our parents eventually bring home a baby." (Hiding the number of attempts, the cost, and the time.)

- "We've helped thousands of families." (In what timeframe, with what outcomes?)

- "We've never had a failed journey." (Not possible.)

- Any framing that implies the agency itself is responsible for the live birth rate.

A Final Word

The six traps above are not hypothetical. Every one of them is something we've watched happen to intended parents who came to Ivy after something went wrong at another agency. The same mistakes keep happening because the information that would prevent them is hard to find unless you already know where to look.

Take the consultation questions to every agency on your shortlist. You're not looking for the warmest sales call or the most reassuring answer — you're looking for the most specific one. Specific names, specific policies, specific numbers. A vague answer is itself an answer. If Ivy is on your shortlist, we welcome every question above; we've written full articles on four of them, so you can read our answers before you even schedule a call.

FAQ

1. When should a surrogacy agency charge the agency fee?

At the very earliest, after you've been matched with a specific surrogate candidate. Ideally, only after that candidate has cleared both medical and psychological screening. Any agency that asks for the full agency fee at signing — before you've seen a profile or been matched — is asking you to give up your financial leverage in exchange for a spot on a waiting list.

2. Who should review a surrogate's medical records before she's matched with an intended parent?

Someone on the agency's own team with clinical training, before the records ever reach the IVF doctor. This internal pre-screening catches the kinds of details that only reveal themselves to a trained reader — a complicated prior pregnancy, a chronic condition whose management record tells a different story than the summary line, subtle findings in a delivery note that predict a higher-risk future pregnancy. Catching these on day one prevents failed matches weeks or months later. If an agency has no one qualified to read medical records, they are outsourcing the risk of failed screening to you.

3. If I need a re-match, will I be prioritized over new clients?

At a well-run agency, yes. Re-match clients should get first access to newly available surrogates, because they have already waited, already paid, and already absorbed the cost of a failed match. Agencies that put re-match clients "in the same queue" as new clients are quietly prioritizing new revenue over existing journeys. Ask for the agency's actual re-match policy and the average re-match waiting time over the past 12 months — an agency that truly operates on re-match priority will be able to answer both.

4. Should I avoid surrogacy agencies with in-house legal or in-house escrow?

Yes, on both counts. In-house legal is a conflict of interest and, in states like California, a direct violation of independent-counsel requirements. In-house escrow has produced some of the most damaging fraud cases in the history of the U.S. surrogacy industry. Independent legal counsel and independent, licensed escrow are non-negotiable protections.

5. Does a surrogacy agency handle newborn insurance for international intended parents?

Many agencies explicitly do not. This is one of the most important questions for international IPs to ask before signing, because the cost of missing the newborn-insurance purchase window (usually 28–30 weeks of gestation) can reach six figures if the baby needs NICU care. A professional agency will introduce insurance planning at the very first consultation and connect you with licensed insurance brokers long before the transfer cycle.

6. How do I evaluate a surrogacy agency's success rate claims?

Be skeptical of any dramatic number. Most high advertised rates (95%, 99%, etc.) are measuring the cumulative outcome across unlimited attempts — "did you eventually bring home a baby" — not the likelihood any given transfer or cycle will succeed. For reference, a 2025 U.S. multicenter study in F&S Reports analyzing 15,013 single euploid frozen embryo transfers found a per-transfer live birth rate of 55.8% for intended parents aged 35–37 using their own eggs, declining with age from there. Any per-transfer or per-cycle number above that is mathematically incompatible with the biology. More fundamentally, success rates in surrogacy are not really about the agency at all — they're determined by the intended parents' (or donor's) age at egg retrieval, the IVF doctor and embryology lab the IP chose, and the genetic quality of the embryos. Every gestational surrogate who reaches a transfer has, by definition, already met the IVF clinic's medical criteria. An agency willing to misrepresent this in marketing is telling you something important about how it will communicate with you for the next 18 to 24 months.

Disclaimer

The operational practices, fee structures, and marketing language described in this article reflect general patterns observed across the U.S. surrogacy industry. They are not directed at, and should not be read as referring to, any specific agency. Clinical and statistical figures cited above are drawn from peer-reviewed research and publicly available data published by the U.S. Centers for Disease Control and Prevention (CDC), the American Society for Reproductive Medicine (ASRM), and F&S Reports. This article is intended as general educational information for intended parents and does not constitute legal, medical, financial, or insurance advice. Readers considering a surrogacy journey should consult licensed professionals in each relevant field before making any decisions.