🧩 Key Takeaway

Your surrogacy journey is a deeply emotional and financial commitment. Never compromise on transparency or fund safety. Always choose an agency that uses a licensed, independent escrow or attorney-managed trust account—and make sure you transfer funds directly to that account, not through the agency.

Introduction

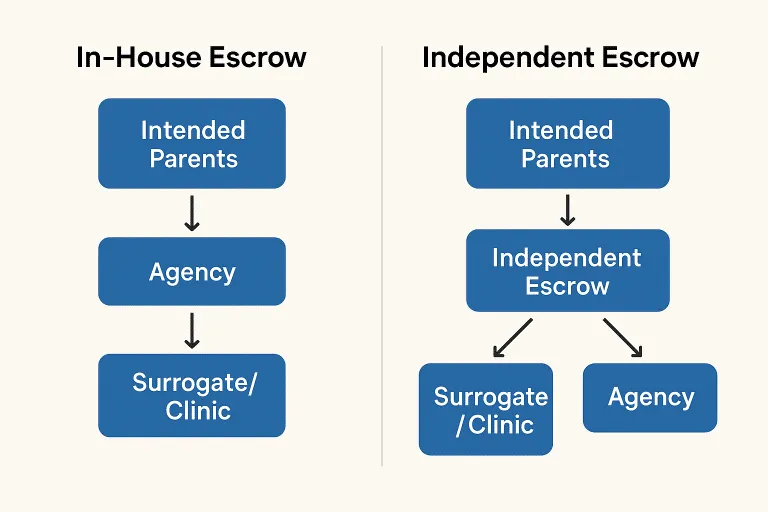

When choosing a surrogacy agency, one of the most overlooked yet crucial aspects is how your funds are held and managed. Some agencies use an in-house escrow account, meaning they directly control the money meant to pay the surrogate, medical bills, and other related expenses. While this might seem convenient, it can expose intended parents to serious financial and ethical risks.

Understanding the difference between independent escrow, trust account, and in-house escrow—and how each operates—is key to protecting your investment and peace of mind throughout the surrogacy journey.

What Is an Escrow or Trust Account in Surrogacy?

An escrow or trust account is a secure, third-party account where intended parents deposit the funds required for the surrogacy process. The escrow or trust provider disburses payments according to the contract—covering the surrogate’s compensation, medical bills, legal fees, and other agreed expenses.

The purpose is to protect both intended parents and surrogates, ensuring all payments are made properly, on time, and in compliance with the surrogacy agreement. These accounts are typically managed by:

- A licensed escrow company, regulated by the state’s financial department, or

- An attorney-managed trust account, overseen by state bar association rules.

Both offer strong legal safeguards when used correctly.

The Problem with In-House Escrow

1️⃣ Conflict of Interest

When an agency both manages the surrogacy process and controls the escrow account, a clear conflict of interest arises. The agency decides when and how funds are released, meaning it can prioritize its own financial needs over client protection. If a dispute occurs, the agency cannot act as a neutral party—defeating the purpose of escrow or trust altogether.

2️⃣ Lack of Oversight and Regulation

Independent escrow companies and attorney trust accounts are licensed, bonded, and audited under strict legal frameworks. In contrast, in-house escrow accounts often operate without external supervision, meaning there is no guarantee that:

- Funds are held separately from the agency’s operating accounts

- Payments follow the contract accurately

- Records are reviewed by independent auditors

This lack of regulation increases the risk of mismanagement or misuse.

3️⃣ Risk of Misuse or Insolvency

Unfortunately, the surrogacy industry has seen cases where agencies used escrow funds for operational expenses or went bankrupt—leaving intended parents unable to recover their money. If your funds are held in an agency’s internal account, they could become part of its assets during insolvency, putting you at serious financial risk.

4️⃣ Reduced Transparency

Licensed escrow and trust providers offer detailed statements and online access, allowing you to monitor every transaction. In-house escrow systems lack these safeguards, leaving intended parents with limited visibility into how and when their money is used.

5️⃣ Potential Legal Noncompliance

States such as California and Nevada require that surrogacy funds be held by an independent, licensed escrow or attorney-managed trust account. If an agency uses in-house escrow, it may be violating these laws—creating potential legal exposure for clients.

Why Independent Escrow or Trust Accounts Are Safer

Choosing a licensed independent escrow or trust account gives intended parents peace of mind. It ensures:

- Regulated, insured fund management

- Separation between agency operations and client funds

- Transparent and traceable financial records

- Compliance with state surrogacy regulations

- Neutral handling in case of disputes

Whether funds are managed through an independent escrow or an attorney-managed trust account, the key is ensuring your money remains under a licensed third party’s custody, never under the agency’s control.

⚠️ Even Independent Escrow Can Fail—If Used Incorrectly

Having an independent escrow company or trust account does not automatically guarantee safety—it depends on how funds are transferred.

In one real industry case, a surrogacy agency claimed to use an independent escrow provider. However, instead of asking intended parents to wire funds directly to the escrow or trust account, the agency requested the money be sent first to its own business account, promising to forward it later.

The result was devastating: the agency never transferred the funds and misappropriated the money intended for surrogate compensation. When the agency collapsed, those funds were unrecoverable.

👉 The lesson is clear:

Even when an independent escrow or trust account is in place, intended parents should always send funds directly to that account, never through the agency. This ensures your money is legally protected and fully traceable.

🧯 A Lesson from the Industry: The SurroGenesis Escrow Scandal

One of the most notorious cases in U.S. surrogacy history clearly illustrates the dangers of mishandled funds — the SurroGenesis escrow fraud.

In 2009, a California-based agency called SurroGenesis claimed to offer secure financial management for intended parents through its in-house escrow structure. In reality, the company’s founder, Tonya Collins, embezzled over $2 million in client funds that were meant to pay surrogates and medical expenses. The money was diverted into her personal accounts and spent on luxury goods, vacations, and personal expenses.

When the fraud was uncovered, SurroGenesis went bankrupt, leaving numerous intended parents and surrogates with devastating financial losses. Collins was later convicted of mail fraud and sentenced to federal prison.

The case became a turning point for California’s surrogacy legislation — directly influencing the enactment of California Family Code § 7961, which now requires all non-attorney surrogacy facilitators to hold client funds in a licensed, independent escrow company or attorney-managed trust account.

🔹 Further Reading: California Family Code § 7961 (Official Text) FBI Case Summary – United States v. Tonya Collins (2013)

👉 This case remains a powerful reminder: even when an agency promises financial security, no system is safe unless funds are truly managed by an independent, licensed escrow or attorney trust account.

🧾 Why Some Large Agencies Still Use In-House Escrow

You might wonder why some of the biggest surrogacy agencies in the U.S. still manage funds in-house—even though it carries obvious risks. The reasons often come down to regulations, revenue, and control.

1️⃣ Regulatory Gaps

Not all states require surrogacy funds to be held by a licensed independent escrow or attorney trust account. In states without strict rules, large agencies can legally run in-house escrow divisions or “sister companies,” allowing them to handle client money internally.

2️⃣ Extra Profit

By managing escrow themselves, agencies can collect management fees instead of paying a third-party provider. For high-volume agencies, this becomes a lucrative additional income source.

3️⃣ Cash-Flow Flexibility

Controlling funds directly allows agencies to adjust payment timing—drawing fees early or delaying reimbursements as needed. While convenient for them, it reduces transparency and increases risk for intended parents.

4️⃣ Market Power

Because of their strong brand reputation and large client base, these agencies can persuade clients that internal systems are “safe enough.” But reputation doesn’t equal regulation—no in-house escrow can replace independent oversight.

👉 In short:

Big agencies keep in-house escrow not because it’s safer, but because they can—and it’s profitable. True financial protection comes only when funds are held in a licensed independent escrow or attorney-managed trust account, completely separate from the agency.

🏛 Ivy Surrogacy’s Approach: Full Transparency, No In-House Escrow

At Ivy Surrogacy, we believe financial integrity is the foundation of trust. That’s why we will never use an in-house escrow system.

Our financial structure protects both intended parents and surrogates at every stage:

- Independent Escrow or Attorney Trust Account Only We exclusively work with licensed third-party escrow companies or attorney-managed trust accounts that meet all state regulatory requirements. Ivy Surrogacy has no control or access to these accounts.

- Two Separate Financial Channels

- Optional Full Escrow Funding Intended parents may also choose to deposit all funds—including the agency fee—into the independent escrow or trust account. The licensed provider then disburses Ivy’s agency fees according to the agreed retainer schedule.

This transparent, compliant system ensures 100% fund security and accountability for every family we serve.

📘 FAQ

1. What is an escrow or trust account in surrogacy?

It’s a secure third-party account—managed by a licensed escrow company or attorney—that holds intended parents’ funds for surrogate compensation, legal fees, and medical expenses. It ensures fairness and compliance.

2. Why is in-house escrow risky?

Because the agency directly controls your funds, it creates conflicts of interest, reduces oversight, and exposes you to financial risk if the agency mismanages or mixes funds.

3. Is independent escrow or trust account required by law?

Yes, in many states like California and Nevada, surrogacy funds must be held by an independent licensed escrow or attorney-managed trust account to comply with surrogacy laws.

4. Can independent escrow or trust account still fail?

Yes—if funds are sent to the agency instead of directly to the escrow or trust provider. Always wire money directly to the licensed third-party account for full protection.

5. Why do some agencies still use in-house escrow?

Because not all states regulate escrow practices strictly, and large agencies can profit from internal management fees and cash-flow flexibility. However, it still exposes clients to unnecessary risk.

6. How does Ivy Surrogacy handle surrogacy funds?

Ivy Surrogacy never uses in-house escrow. We work only with licensed independent escrow or attorney trust accounts, ensuring transparency, state compliance, and client fund safety.